The Global Audit Software Market is gaining significant momentum as organizations worldwide adopt digital solutions to improve compliance, manage risk, and streamline internal and external auditing processes. Audit software enables businesses to automate workflows, track financial transactions, identify irregularities, and ensure adherence to regulatory standards. The growing complexity of business operations, rising compliance demands, and the shift toward digital transformation are fueling the adoption of advanced audit solutions. The global audit software market size was valued at USD 2.06 billion in 2024 and is expected to reach USD 5.97 billion by 2032, ****at a CAGR of 14.20% during the forecast period. As businesses across industries seek greater transparency, efficiency, and accuracy in auditing, audit software is becoming a cornerstone of governance, risk management, and compliance strategies.

The Audit Software Market is being shaped by strong growth drivers. Organizations are under increasing regulatory scrutiny, with governments and international bodies enforcing strict compliance standards across sectors such as banking, healthcare, energy, and manufacturing. Audit software provides real-time monitoring, risk detection, and reporting tools that help businesses stay compliant and avoid costly penalties.

Digital transformation is another major driver. As businesses migrate operations to cloud platforms and adopt digital workflows, the need for scalable, automated audit solutions has grown. Audit software integrates seamlessly with enterprise systems, offering data analytics, AI-powered anomaly detection, and mobile accessibility for auditors.

Challenges in the market include high implementation costs, particularly for small and medium enterprises (SMEs), and the complexity of integrating audit software with legacy systems. Cybersecurity risks are also a concern, as sensitive financial and operational data must be protected. However, opportunities lie in the development of cloud-based, subscription-driven audit software models that lower upfront costs, as well as in expanding adoption across emerging economies with growing regulatory frameworks.

The Global Audit Software Market can be segmented by deployment model, component, organization size, and end-user industry.

By deployment model, the market is divided into on-premises and cloud-based solutions. While on-premises solutions remain relevant for organizations with strict data control requirements, cloud-based software is growing rapidly due to its scalability, cost-effectiveness, and ease of access.

By component, the market includes software and services. The software segment dominates with solutions for financial audit, operational audit, compliance audit, and IT audit. Services, including implementation, consulting, and support, are also vital as organizations seek guidance in integrating and optimizing their audit systems.

By organization size, large enterprises represent the majority of demand, driven by their complex operations and regulatory compliance needs. However, SMEs are emerging as a fast-growing segment, particularly with the availability of affordable, cloud-based solutions tailored for smaller businesses.

By end-user industry, key segments include banking, financial services, and insurance (BFSI); healthcare; IT and telecom; energy and utilities; manufacturing; government; and retail. BFSI leads due to stringent financial regulations, while healthcare is growing quickly as patient data and regulatory compliance take center stage.

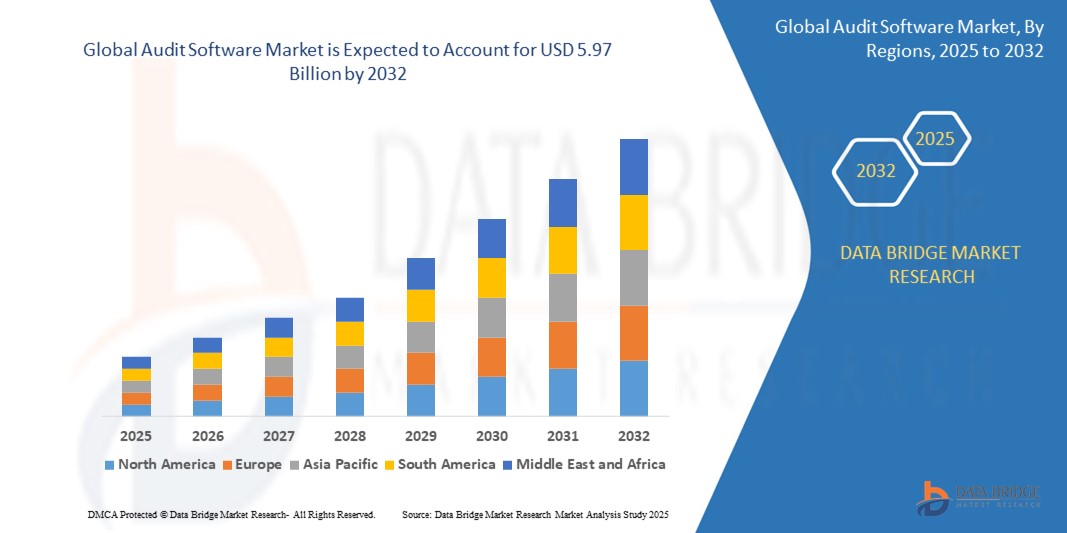

Regionally, the Audit Software Market demonstrates diverse growth patterns.

North America dominates the market due to the presence of leading software vendors, strong regulatory frameworks, and rapid adoption of advanced technologies. The United States, in particular, has a mature audit culture with widespread use of digital solutions in both private and public sectors.

Europe follows closely, driven by strict compliance standards such as GDPR and financial regulations that necessitate transparent auditing. Countries such as the UK, Germany, and France are key contributors to regional growth.

Asia-Pacific is the fastest-growing region, with countries like China, India, and Japan witnessing increased adoption of audit software. Expanding business ecosystems, government digitalization initiatives, and rising awareness of compliance are propelling growth in this region.

The Middle East and Africa are gradually adopting audit software, particularly in financial institutions and government sectors that demand high transparency. South America is also experiencing growth, with Brazil leading adoption due to regulatory pressures and modernization of financial systems.